This report provides a detailed analysis of Chiplet market trends, patent filings, and top players involved in Chiplet technology development. The results indicate significant potential for the Chiplet industry in the years to come.

The technology overview provides a detailed introduction to Chiplets, including their benefits over traditional monolithic chips and the evolution timeline of Chiplet technology in key application areas.

The report highlighted key market insights, including market value and forecasting, emerging startups, recent partnerships and mergers, acquisitions, regulatory drivers, and standards related to the technology.

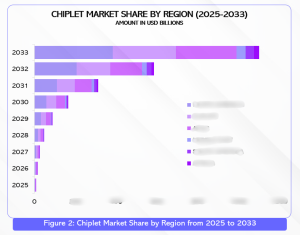

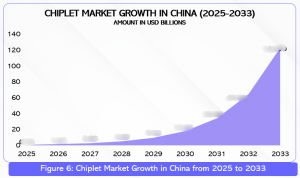

The market is expected to grow at an exceptional CAGR of above 88% from 2025 to 2033, reaching a total market value of USD 1142.1 billion.

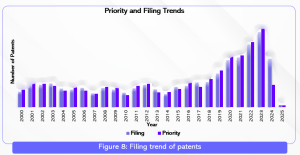

The filing trend for Chiplet technology saw consistent growth from 2015 to 2023. This period marks the most significant number of patent filings, indicating a notable boost in the development of Chiplet technology during this phase.

The regional analysis of the Chiplet industry revealed that North America held the largest market share, accounting for 37% of the global revenue, with a market size of USD 2.6 billion in 2025. The growth in North America is driven by the presence of major technology hubs and a strong demand for advanced computing solutions.

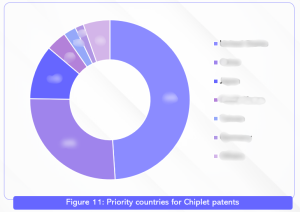

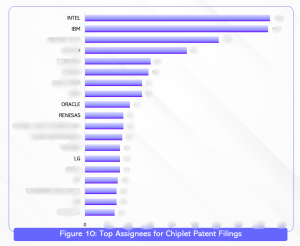

As many as 1,495 distinct assignees filed patents related to Chiplet technology. Among priority countries, the US holds the largest share in total filings, showcasing the origin of companies innovating in Chiplet technology.

The patent filings are further categorized into eight key application areas, namely Telecommunications, Healthcare, Wearable Devices, Display Devices, High Computing, Automotive, Consumer Electronics, and IoT.

To better understand the long-term viability of the businesses operating in the Chiplet space, we have performed Porter’s 5 forces analysis. The analysis examines the intensity of competition, the bargaining power of buyers and suppliers, the threat of new entrants, and the existence of substitute products. The Porter’s five forces analysis reveals a high competitive rivalry in the industry due to the presence of semiconductor giants.

The patent filing trend exhibits consistent growth from 2015 to 2023. More than 43% of overall patent applications were filed during this period.

Major semiconductor manufacturer Intel is the top patent assignee in the list. Furthermore, the distribution analysis for the application domain reveals that more than 33% of patents have applicability to the telecommunication sector, underscoring the importance of Chiplets in processing large volumes of data and addressing integration challenges in the industry.